The Strait of Hormuz has been closed to normal maritime traffic for more than two weeks, triggering the most severe disruption to global energy supplies in modern history and sending crude prices surging to nearly $120 per barrel. The closure — the first in the strait’s history as a critical international waterway — follows a military conflict between Iran, the United States, and Israel that has included direct attacks on oil infrastructure across Saudi Arabia, Kuwait, and the United Arab Emirates.

Several vessels have been struck in the strait since hostilities escalated, and the disruption was compounded early on by the need to renegotiate insurance contracts for oil tankers attempting passage. Roughly 20 percent of the world’s petroleum and nearly a fifth of global liquefied natural gas transits the narrow chokepoint each year, making it the principal gateway for Gulf Cooperation Council states to international markets. A complete cessation of Persian Gulf oil exports would remove close to 20 percent of global supply — a shortfall that dwarfs every comparable geopolitical shock of the past half-century.

For context, the Yom Kippur War of 1973 removed just over 6 percent of global oil supplies from the market. The Iranian Revolution of 1979, the outbreak of the Iraq–Iran War in 1980, and the Persian Gulf War of 1990 each removed no more than 6 percent. The current crisis has no historical precedent in scale.

The economic fallout is already cascading across producer nations. Iraq, the world’s sixth-largest oil producer, cut output at Basra by 70 percent — from 3.3 million barrels per day to just 900,000 — while redirecting 170,000 barrels per day through a pipeline to Turkey. Saudi Arabia, the world’s second-largest producer, shuttered the Ras Tanura refinery in early March, taking 550,000 barrels per day of processing capacity offline, and rerouted remaining production through the East-West pipeline to Yanbu port on the Red Sea. The UAE similarly closed its largest refinery and pivoted to overland pipeline routes. Iraq and Kuwait both began curtailing production in early March 2026.

Major energy companies moved swiftly to limit contractual exposure. Qatar Energy, Shell, Kuwait Petroleum Corporation, and Bapco all invoked force majeure clauses across GCC countries. Qatar, the world’s second-largest LNG exporter, halted LNG production entirely — a decision with severe consequences for Asian importers. Qatar and the UAE together supply 30 percent of China’s LNG imports, 53 percent of India’s, 72 percent of Bangladesh’s, and 14 percent of South Korea’s. Approximately 80 percent of all Persian Gulf oil exports are destined for Asian markets, meaning the continent bears a disproportionate share of the supply shock.

Gas markets in Europe have also been rattled. British wholesale gas prices more than doubled, while Dutch benchmark prices rose 24 percent. Asian LNG benchmark prices jumped nearly 39 percent in early March alone.

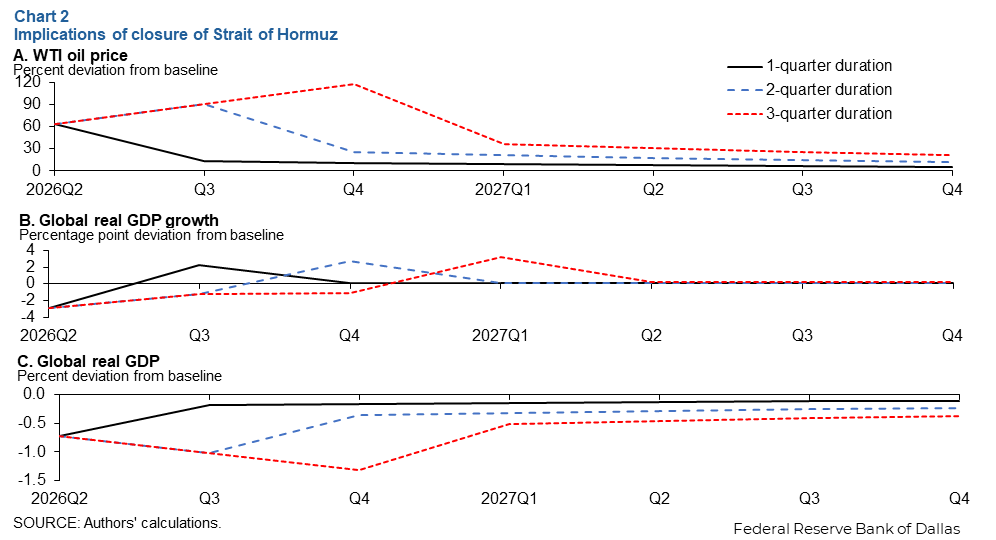

Modelling by the Federal Reserve Bank of Dallas offers a sobering projection of the crisis’s trajectory. Assuming the strait remains closed through the second quarter of 2026, average West Texas Intermediate crude prices are expected to reach $98 per barrel for that period — though spot prices have already exceeded that threshold. If the closure extends to three quarters, the probability of the strait remaining shut through the third quarter of 2026 stands at 58 percent, falling to 35 percent for the fourth quarter.

The closure raises acute questions of international law. Article 38 of the United Nations Convention on the Law of the Sea, adopted in 1982, guarantees ships and aircraft the right of transit passage through straits used for international navigation. Article 44 explicitly prohibits coastal states from hampering or suspending that right. The principle was affirmed even earlier by the International Court of Justice in the landmark Corfu Channel case of 1949. The 1994 San Remo Manual on International Law Applicable to Armed Conflicts at Sea further stipulates that neutral vessels retain the right to transit international straits during armed conflict.

Whether those legal frameworks can be enforced in the current environment remains deeply uncertain. The GCC Vision for Regional Security, adopted at the bloc’s 158th session in Doha in December 2023, envisioned cooperative mechanisms to protect critical maritime infrastructure — mechanisms that have so far proved insufficient to prevent the crisis from unfolding. With no clear timeline for a ceasefire and insurance markets still pricing in extreme risk, the world’s most strategically vital waterway remains effectively closed, and the full economic consequences are still taking shape.